The Company Brain: How a VC Fund Runs Itself on AI Agents

If you run a small fund, you already know the feeling: you are the bottleneck. Everything your fund knows lives scattered across your inbox, your Slack, ten different tools, and your own head. Every founder you met, every deck, every note, every intro thread. And you can only act on a sliver of it. Deals go cold. Follow ups slip. You rediscover things you already knew last month.

We spent the last few months sitting down with VC friends and mapping where their weeks actually go. Then we built the thing this post describes. It runs live today on real companies. There is a 4 minute demo embedded below.

What is a company brain?

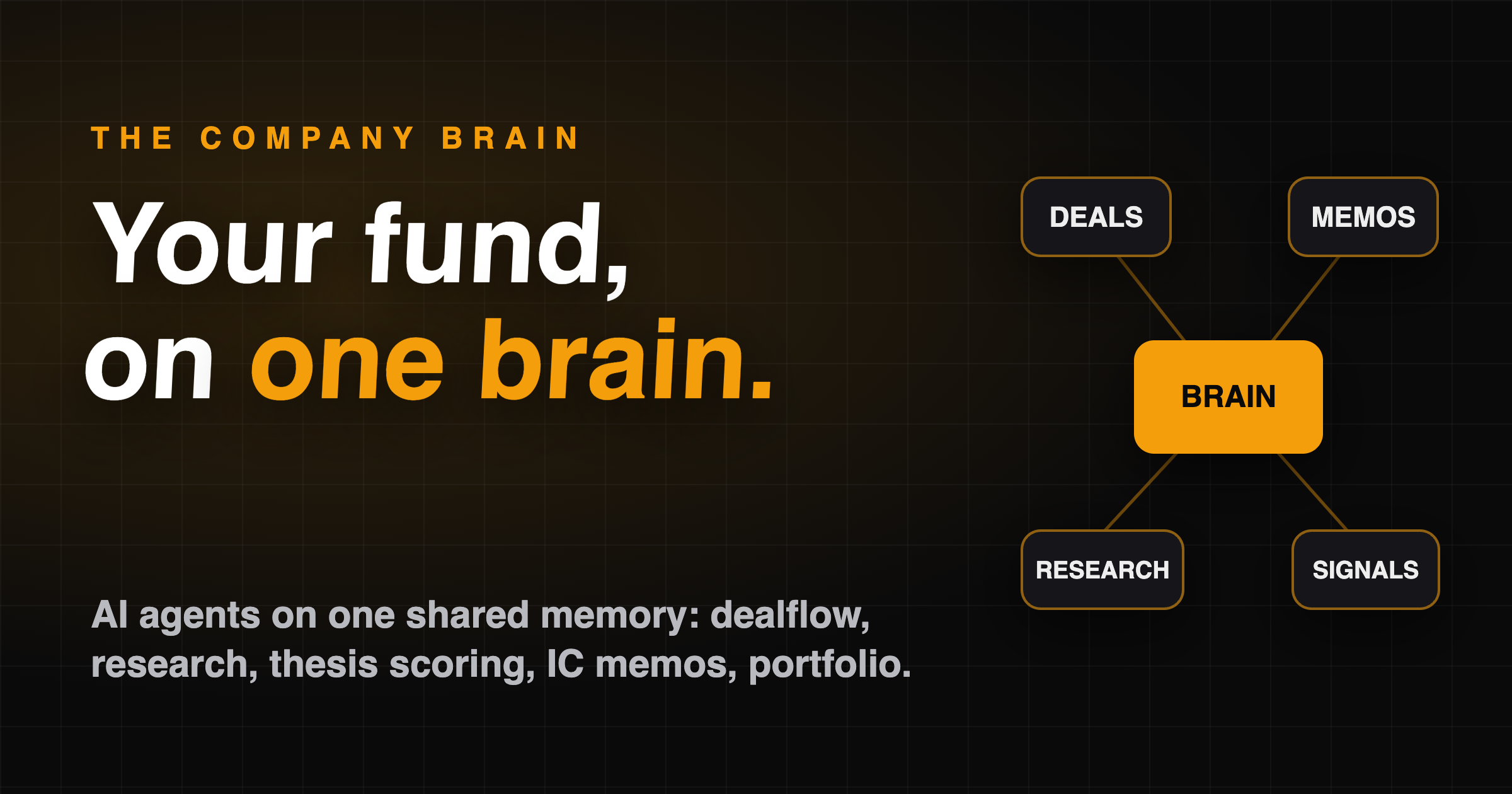

A company brain is one shared memory that holds everything your organization knows, with AI agents that read that memory and do real work on top of it. Not a chatbot that answers questions. Agents that act: research, score, draft, monitor, file.

The definition matters because of what it excludes. A CRM is not a company brain; it holds contacts, not knowledge. A note taking tool is not a company brain; it holds text nobody rereads. A chat assistant is not a company brain; it forgets everything the moment you close the tab. The test is simple: does the system remember everything your fund knows, and does work happen on top of that memory without you?

Why another tool will not fix a fund

The average small fund already pays for eight to twelve tools: a CRM, a notes app, a data provider, a scheduling tool, a portfolio tracker, and so on. Each one holds a slice of what the fund knows, and none of them talk to each other. That is the actual problem. The knowledge is fragmented, so every decision starts from a partial picture, and the partner becomes the integration layer. The bottleneck is structural, not personal.

An AI agent with no memory of your fund is just a chatbot with extra steps. That line is the whole argument. Intelligence without your context produces generic output: deals scored on hotness instead of fit, memos that read like press summaries, follow ups that miss history. The fix is not a smarter model. The fix is memory.

The two moves

Everything we build for a fund comes down to two moves.

Move 1: load the knowledge. Before any agent runs, you feed the brain everything the fund already knows. Documents, email, Slack history, past deals. And the thing that usually lives only in the partners’ heads: the investment thesis. What you back, what you pass on, the must haves, the deal breakers, the weights. It all becomes one shared memory that every agent reads before it does anything.

Move 2: a module per workflow. A module is one job the fund does, handed to agents that run it on top of the brain. Deal intake is a module. Research is a module. LP updates, diligence, market maps, reference calls: each one can be a module. Snap one in, it runs on the brain. Snap in another and they compound, because they share the same memory instead of fragmenting it further.

What the dealflow module does, end to end

The first module we built handles the job every single VC we talked to complained about: turning inbound deals into decisions.

- Intake. Deals arrive from anywhere: your inbox, a founder filling a form, a scout agent watching YC batches and GitHub. Everything lands in one pipeline. Nothing gets dropped, nothing gets logged twice.

- Research. The moment a deal lands, an agent researches it into an analyst grade dossier: founders, market, competition, traction, cap table, a diligence plan. Every claim is sourced. No human typed any of it.

- Thesis scoring. The agent scores the deal against the fund’s actual thesis, because it read the thesis. The question it answers is “is this for us,” not “is this hot.”

- IC memo. It drafts the investment committee memo with the risks at the top. On one live deal it caught a risk the founder’s deck had buried: the top two customers were 40 percent of revenue. That flag was at the top of the memo before anyone had opened a single slide.

- Portfolio monitoring. It watches the companies the fund already backed for key hires and competitor moves, and it keeps the record current on a schedule.

We left the system alone for a few days as a test and came back to a week of associate work, already done.

Here is the whole thing running live, in four minutes:

One module is about 10 percent of a fund

When we mapped workflows with these funds, dealflow turned out to be roughly a tenth of what a fund actually does. LP updates, capital calls, diligence, market maps, fund admin, reference calls, portfolio support. Every one of those is a candidate module, on the same brain.

That is the real difference between this and buying another tool. Tools fragment knowledge; modules compound it. Each new module makes every existing module smarter, because they all read and write the same memory. The end state is a fund where the institutional knowledge is the system, not the bottleneck partner, and the work runs on top of it. Completely, one module at a time.

The deeper bet: in a few years, the funds that win competitive deals will not be the ones with the most tools. They will be the ones whose memory compounds. Every deal, every memo, every decision feeding the next one. A new tool can be bought by anyone. A fund’s accumulated memory cannot.

Building one for your fund

We build these with funds directly at hebbs.ai. The process is the two moves above: we ingest what your fund already knows, then automate your workflows one module at a time, starting with the one that hurts most. If you want to see where it would fit, tell me the one workflow you would hand off first: parag@hebbs.ai.

FAQ

What is a company brain? One shared memory holding everything an organization knows (documents, email, Slack, theses, history), with AI agents that read it and execute real work: research, scoring, drafting, monitoring. The defining property is that work happens on top of organizational memory, not in disconnected tools.

How is a company brain different from a CRM or a dealflow tool? A CRM stores structured records you maintain by hand. A company brain ingests everything the fund knows, including unstructured knowledge like email threads and the investment thesis, and agents act on it autonomously. The CRM is one possible view of the brain; it is not the brain.

Can AI agents really score deals against an investment thesis? Yes, if the thesis is loaded as explicit, structured knowledge: what the fund backs, what it passes on, the weights, the deal breakers. The agent then scores fit rather than hype. In live use this also surfaces buried risks; in one case, customer concentration of 40 percent of revenue that a deck had not highlighted.

How does a fund start building one? Two moves. First, ingest the fund’s existing knowledge: documents, email, Slack, the thesis. Second, pick a single workflow and turn it into a module run by agents on that memory. Dealflow intake and research is the most common starting point because the pain is daily and the output is easy to verify.

If this was useful, follow me on X for more.

Follow @paragarora on X